International Workplace Group (IWG) Thesis

IWG: International Workplace Group, IWG LN, Price: £1.83, Date: 2nd June 2024.

Disclaimer: This is for informational purposes only, nothing is investment advice, Do your own due diligence. I am often wrong. I am a shareholder of IWG.

History / Overview

International Workplace Group (IWG) is the global leader of flexible office and co-working space. It serves millions of users across 3,500+ locations and 120 countries, leveraging a portfolio of 19 brands, including Regus, Spaces, Signature, and HQ. IWG’s scale is notable, with more locations and system revenue than the other top 10 competitors combined. According to Fortune Business Insights, the global flexible office market was c.$35bn in 2023, and is expected to grow to $96bn in 2030 (16% CAGR), as organisations embrace hybrid working that saves money, and increases employee satisfaction. The company was founded in 1989 by Mark Dixon who still serves as CEO and retains a 25% ownership stake.

From 2010-19 the company delivered impressive growth. Revenue CAGR was double digit, while FCF pre growth capex / share and total shareholder return CAGR were both over 20%. However, the model was both operationally geared and capital intensive, with new location capex spend eating up most of cash flow from operations.

In 2019, the company focused on franchising. It sold its Japanese and Swiss operations for 14-15x EBITDA and secured go-forward franchise agreements. Investor hopes were building that similar transactions would be forthcoming in the UK / US to crystallise substantial value for shareholders but these efforts were curtailed by the painful impact of covid. In 2022, IWG pivoted its focus towards growing via management contracts (which I will dig into in the “Thesis” section) and acquired The Instant Group to beef up its digital business, now called Worka.

Worka is “the largest independent global marketplace for flexible workspace”. It’s a mix of consulting, data and marketplace services (booking.com for the flexible office industry, with IWG being the anchor ‘partner’). It has its own board, and the medium-term plan remains for this to be independent. Upfront investment is going in via small tuck in acquisitions and platform / software to build out the digital product suite and establish global coverage. Gross margins are c.50%, EBITDA margins are c.40%. Consulting is lower margin, and is a declining share of the mix. 50% of IWG’s virtual office revenues are booked within Worka and make up the largest portion of the revenues for the division. These are very sticky and high margin revenue streams, consistently growing high single digit. In 2023 divisional organic growth was 18% but is expected to be flat this year as a large, but low margin, consulting contract rolled off. Management has stated that ex-the consulting contract impact, underlying organic growth is double digit, and expect that growth trajectory to persist.

The largest profit contributor for the group remains the owned & leased (O&L) estate. This was materially impacted by covid and gross margins are still on their recovery path back to normalised levels of 25% (vs 15.8% in 2022 and 20.4% in 2023). This is now being run for cash, with the estate expected to remain about flat going forwards. There is an opportunity for management to sell the (smaller) owned portion of the estate once normalised profitability is restored. IWG’s, a bit like Ryanair, are industry leaders in driving ancillary revenues (25-30% at IWG locations vs single digit at Wework), while also leveraging its scale to achieve cost efficiencies unattainable to its competitors. For example, they are the second larger purchaser of office furniture globally, after the US government). Most of the estate is leased, and over 95% of these leases either are housed within remote SPV structures, without recourse to the parent, or have break clauses enabling the company to exit its leases within 12-months. This has been critical for IWG to exit or restructure terms at unprofitable locations, in contrast to Wework.

Latest News / Entry Point

IWG’s stock has been under pressure since the announcement on 29th May that Mark Dixon, reduced his ownership from 28% to 25%. While insider selling is never a positive, I don’t see this as a cause for concern. Mark Dixon has business interests outside of IWG (e.g., investing in vineyards) and with IWG stopping dividend payments during covid, his desire for liquidity to fund some of these passion projects is understandable. He had previously done this via a margin loan, which made several shareholders uneasy. The stock sale allowed him to repay and terminate the margin loan. Also, Wework’s recent recapitalisation and exit from bankruptcy, has raised fresh competition concerns.

Competitive Threat / Wework

Wework is currently a $2bn revenue business with 330 locations and, based on their business plan, is targeting being adjusted EBITDA positive in H2 2024 and FCF positive in 2025. When Wework was in “growth at any cost” mode, their lack of financial discipline drove down industry returns. But times have changed. Capital is no longer free, credit funds have replaced VC dreamers on the register, and the post-bankruptcy business plan is focused on profitability, not growth. A financially disciplined competitor with limited growth ambitions is a good outcome for IWG. Also, Wework’s footprint and experience to-date is focused on larger, premium locations in major global cities. IWG has a portfolio of brands addressing a spectrum of price points, geographically is more thinly spread out with the majority of its expansion coming from suburban locations, and skews more to mass market. Using a hotel analogy – IWG’s has thousands of “Holiday Inns” dotted around, vs Wework that has a few hundred “Crown Plazas” in major global cities. The market size and opportunity are large enough for several operators to profitably coexist. Nonetheless, if you are a landlord looking for a partner to managed a flexible office solution, would you choose IWG, who have a track record of doing it profitably across a multitude of brands / price points / locations over many decades, or Wework, who despite having a strong consumer brand, have a track record of losing money and limited experience outside of major cities centres?

Thesis

IWG is the only globally scaled operator that has a consistent, long term track record of profitably delivering flexible office space across city and suburban locations. It is therefore the primary beneficiary and solution provider for both companies shifting towards more “hybrid” working and the growing number of landlords who are struggling to lease space under the traditional framework of securing a corporate tenant on a long-term lease. Furthermore, most landlords lack the expertise and infrastructure to lease space on a flexible basis and need assistance from a third party to successfully achieve this.

Since late-2022, IWG pivoted its focus towards management contracts and on a go-forward basis has virtually stopped securing new locations under the traditional model. This eliminates their responsibility for the upfront build-out capex costs and committing to pay a landlord a fixed market rate rent on a long-term lease. Now, the landlord pays for all capex and operating costs and IWG provides the brand, infrastructure, supplier terms, marketing, sources the customers and manages the entire operation in exchange for a 16% revenue royalty, under a 10-year contract. The benefit is higher margins, less operational gearing, lower capital intensity, and lower risk. The branded hotel operators (Marriott / Hilton / IHG) provide a clear example of how this model can generate exceptional long term shareholder returns and command high multiples (over 15x EBITDA and over 20x FCF).

For context, in 2019 net growth capex was $465m and in 2024 it should be 85% lower at ~$65m. This is against a backdrop of management guiding to delivering record new location signings and openings. From signing a partner, it takes on average, 10 months to open a new location and another 18 months to hit revenue maturity. Details on this were shared at the December CMD, and the impact of the growing managed partnership pipeline, are about to start flowing through the financials in a meaningful fashion as more locations open and mature. Given momentum on signing managed partners started in late 2022, late 2024 is when FCF should start ramping meaningfully.

Drastically reduced capital intensity, growing contribution from royalty revenues with 100% gross margins, growth from Worka with 50% gross margins, margin recovery within owned and leased to normalised 25% gross margin, relatively fixed overheads, sustainably low-teens cash tax rate courtesy of billions of US NOLs, and working capital tailwinds from deposit inflows as new locations fill up, all contribute to IWG morphing into a FCF machine.

What’s the Catalyst?

1) Making Life Easier for Investors + Rebuilding Credibility

IWG, has historically suffered from the stigma of:

A) UK listed midcap, no close comps, low liquidity => don’t need to care

B) painful accounting => tough to analyse / stock screens badly

C) changing disclosures / KPIs => tough to analyse

D) overpromising and under-delivering => negative earnings momentum

IWG has often been labelled “too difficult”. Its UK midcap status without comps means nobody has to care, and if it’s also difficult to analyse, why bother? What I observe are multiple signs that the company is taking meaningful steps to address this, to be more marketable to investors. Firstly, it hired a very capable IR last year. In the last 12 months the company has done a materially better job at guiding the market conservatively and meeting expectation, helping to build credibility with investors and ending the cycle of earnings downgrades. It has moved to US dollar reporting, removing FX noise. Is widely expected to adopt US GAAP this summer, which will remove a lot of the IFRS lease accounting noise that also contributes to the stock screening very poorly in financial databases such as Bloomberg. At the CMD in December, interestingly hosted in NYC, the company set out its medium-term targets, provided key inputs to help model the managed & franchised (M&F) division, and gave KPIs by division they have committed to not tinker with so that investors can track business performance. Longer term, there’s potential for a US re-listing, which make sense given America is IWG’s largest and fastest growing major market, valuation multiples are higher and liquidity is much better.

2) Buybacks, supercharging FCF / share growth

The key catalyst that I feel the market is ignoring is buybacks. IWG stated at their CMD that they will pivot from deleveraging to shareholder returns as soon as they hit their 1x net debt / EBITDA leverage target, which should happen sometime in Q1 2025. Assuming this comes via buybacks, this can supercharge FCF / share growth as shown in the financial forecasts section.

Financial Forecasts

My forecasts are underpinned by the following key assumptions:

RevPAR: 2% growth, cost inflation: 2% growth

O&L gross margin: 22.5% in 2024, 25% in 2025, and beyond

Worka: revenues flat in 2024, growing ~7% in 2025 and beyond, gross margins at 53%

Capital light signings / year: 117k (in line with 2023 levels), 95% convert to openings

Capital light openings: 9m to open, 18m to hit maturity, at 80% of O&L RevPAR

Royalty rates: franchised 8.5%, managed 16%

Closures: 3% in O&L, 5% in matured M&F

Interest rate: 9%, cash tax rate: 14%

Capex: maintenance $116m, growth: $65m in 2024, growing in line with cost inflation

Leverage pegged at 1x in 2025 and beyond

Buybacks done at 7x FCF (its 2025 FCF multiple)

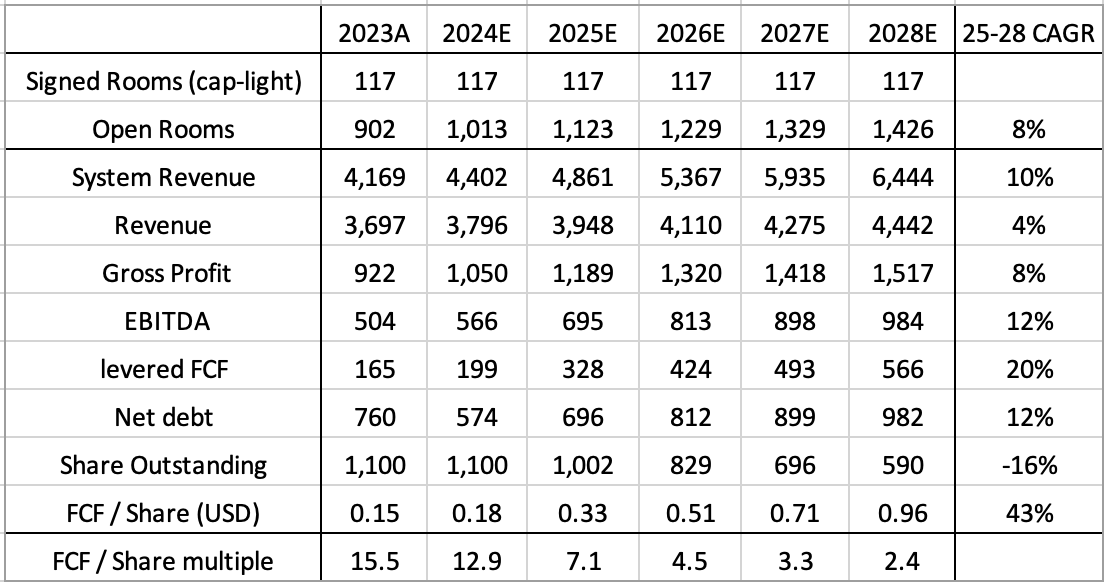

Below are how my forecasts shake out, which dovetails with the company reaching its medium-term target of $1bn of EBITDA in 2028. Note: financials are in USD $m, shares outstanding are fully diluted weighted average, rooms are thousands.

You are paying just c.7x 2025 FCF for IWG, which can grow FCF per share at a 40%+ CAGR (2025 to 2028), if they can keep buying back its stock at its current multiple. This is for a competitively advantaged global leader with a long runway of capital light growth.

The Vistry Playbook

Once IWG activates its buyback, it should be poised to follow a very similar path to Vistry (VTY LN) in September 2023, when it was also: an underfollowed UK midcap, trading on single digit FCF multiple; guided the market to sustainable, multi-year FCF growth while committing to a capital light transition and substantial buybacks. The market took notice, Vistry has been a home run since (+60% in under 9 months), liquidity has drastically improved and it is set to graduate to the FTSE100 in June. I expect IWG to follow a very similar playbook.

What’s the right multiple?

Given how accretive buybacks are at this depressed multiple, I’d be quite happy if a re-rating is “delayed” for many years. The rising contribution from royalties (M&F) and Worka drive improving margins, cash conversion & returns on capital, which is supportive of an on-going re-rating. If IWG was 100% owned & leased, run for cash, with no growth, 10x FCF might be appropriate. If it was 100% royalties & Worka, the pure play managed & franchised hotel operators (Marriott / Hilton / IHG) would be a credible valuation benchmark (15-16x EBITDA, 20-22x FCF). IWG’s fair multiple lies somewhere between these boundaries. By 2028, about half of FCF should be coming from royalties and Worka, as such 15x FCF in 2028 seems perfectly reasonable.

What’s the Upside?

In a no re-rating scenario, the total shareholder return should mirror the FCF/share growth. From Q1 2025, this is a 43% CAGR…. i.e., 2 years is a double, 3 years is a triple. You can make outsized returns even if a re-rating does not happen. If you assume that in 2028, IWG’s multiple re-rates to 15x FCF, that would translate to 500% upside from today’s share price.

There are other additional sources of potential upside: spinning out Worka, a US relisting, accelerating growth in managed partnerships, selling the owned portfolio, and IWG has been on the receiving end of takeover interest multiple times. Any of those would just be icing on an already tasty cake.

Risks

Macro weakness is arguably the biggest risk. This would drive a downdraft in RevPAR and given the operational leverage within the owned and leased estate, would hit the FCF forecasts. However, unless a deep protracted recession takes hold, the micro should trump the macro. Tweaking my assumptions to a no growth macro scenario, from today out to 2028 i.e: flat RevPAR growth, no cost inflation, no owned & leased margin expansion and no growth at Worka, leaves IWG trading on 9x FCF in 2025, with 15% FCF and 28% FCF/share CAGR out to 2028 – still incredibly attractive.

A lot of the thesis hinges on management execution, both operationally but also in terms of capital allocation. With the company generating lots of cashflow, there’s a risk that management decide to find another use for cash which could be riskier (e.g., M&A) and/or less accretive (e.g., deleveraging or dividends). I’m also keeping a close eye on the closure rates, and the cadence of signings and openings within the managed partnership business. The disclosure on Worka is poor, and the 2024 guidance of flattish growth, while credibly explained away as a one off, it was nonetheless a negative surprise and a reminder that’s it’s currently a ‘blackbox’. I do however, expect disclosure to improve with a potential analyst day on the division later this year.

Notwithstanding the risks I’ve laid out above, if management’s medium-term targets and my FCF forecasts, are in the right ballpark and the company follows through with its buyback commitment, IWG, in my opinion, is one of the most asymmetric opportunities in the market today.

Feedback is always welcome.

Uzo Capital

Do you have a comps based on EBITDA multiple? I guess we need to use pre IFRS EBITDA and remove leases from liabilities to come up with the EV. I have around 5.5x currently, not dirty cheap but clearly on the cheaper side

good article, many thanks